OIDCx402 — Seamless payments for receiving digital credentials 🪪

Introduction

Decentralized digital identity has been gaining significant traction over the past couple of years. From European Digital Identity Wallets to Mobile Driver's Licenses, DIDs, Verifiable Credentials, on-chain attestations (EAS), ZKPs, and more, the world is moving closer to portable, verifiable components for identity.

With the x402 hackathon, we asked ourselves: What if we combined decentralized identity with x402? It would make sense for users to easily pay issuers without setting up payment methods for every issuer.

The result is OIDCx402 — a protocol extension that creates a monetization layer enabling seamless micropayments for receiving digital verifiable credentials through OpenID Connect flows.

The Problem: The Missing Monetization Layer

During our years of research, we've extensively reviewed multiple specifications and standards for credential issuance — covering schemas, definitions, technical implementations, and more — but discovered a critical gap: there's no standardized monetization layer for credential issuers.

Credential issuers will inevitably want compensation for their services, yet current standards don't provide any elegant solutions for this particular need. Traditional payment systems create massive overhead — imagine users having to connect payment providers, enter credit card details, and set up accounts with every issuer just to pay $0.45 for four micro-credentials at the end of the month; the friction is absurd.

This payment gap blocks numerous valuable use cases across sectors:

- Healthcare: Instant verification of vaccination status or medical certifications

- Education: Micro-credentials for completed courses, skill assessments, or workshop attendance

- Professional services: Real-time licensing verification for contractors, consultants, or freelancers

- Financial services: Credit score attestations, income verification, or account standing certificates

- AI automation: Agents autonomously purchasing identity proofs, compliance certificates, or access credentials on behalf of users or themselves

This creates an unsustainable economic model where:

- Small-value credentials become economically unviable due to payment processing and setup costs

- Issuers must either absorb losses or inflate prices to cover transaction fees

- Traditional payment flows create poor user experiences

- Potential use cases like AI agents requesting credentials become fundamentally harder to implement and maintain

The lack of a native, low-friction payment layer in credential standards represents a fundamental barrier to the widespread adoption of verifiable credentials (among other challenges). This is where x402 comes in.

Our Solution: OIDCx402

We prototyped OIDCx402 — a seamless integration of the x402 payment protocol into the OpenID for Verifiable Credentials Issuance (OID4VCI) flow. This solution allows for seamless micropayments for receiving digital verifiable credentials through OpenID Connect flows tailored for credential issuance.

Traditional Flow vs. OIDCx402

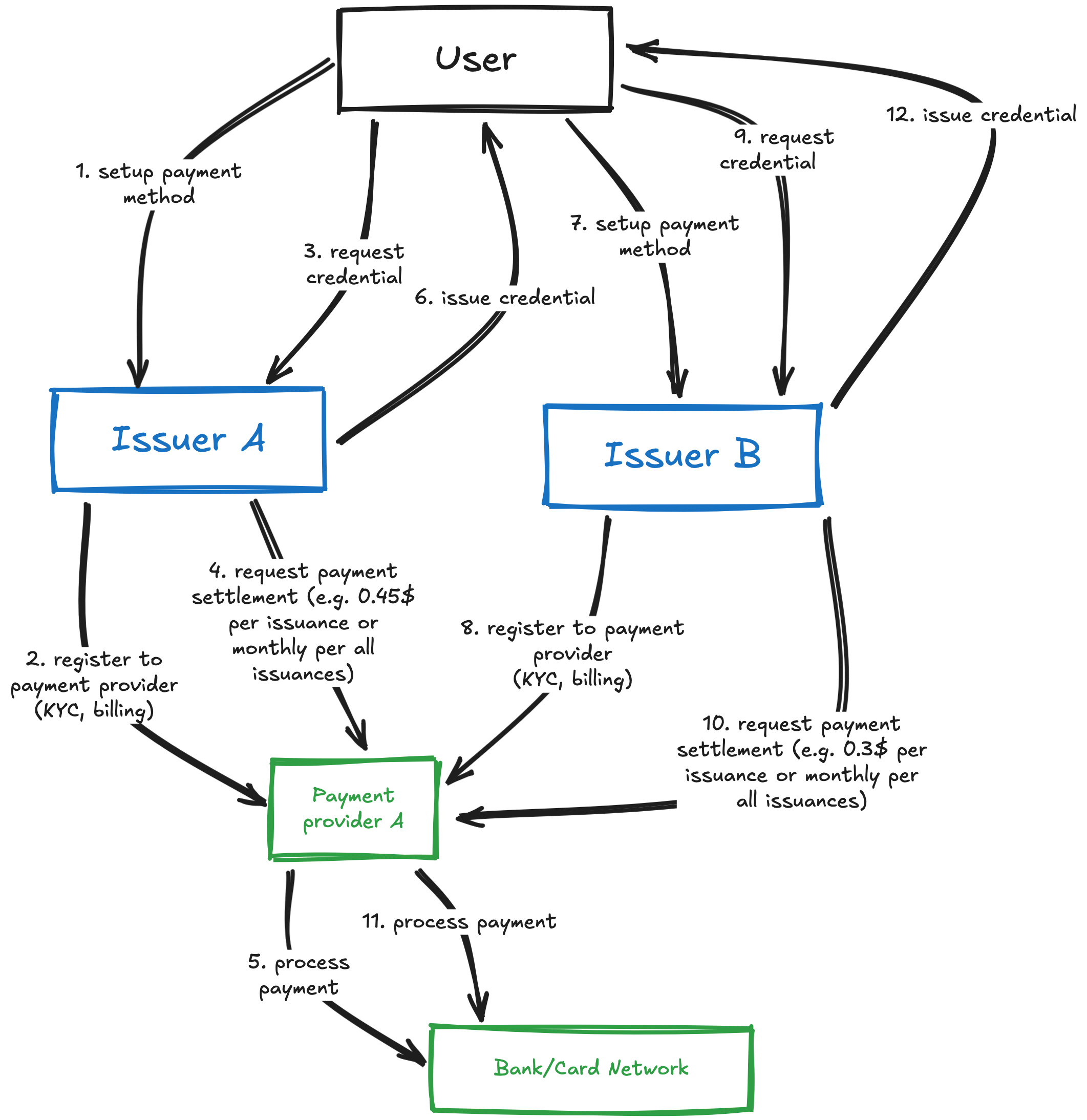

Traditional flow:

In traditional payment flows, users face unnecessary friction. They have to set up their payment methods, enter credit card details, and configure billing separately for each issuer, who often uses different payment providers. All that effort just to pay something like $0.45 once, or at the end of the month, creates excessive overhead for a task that should feel seamless. On top of that, credit card processing fees make micropayments economically impractical. Paying just a few cents often costs more in transaction fees than the payment itself. It’s a broken system for small, seamless payments that should be effortless.

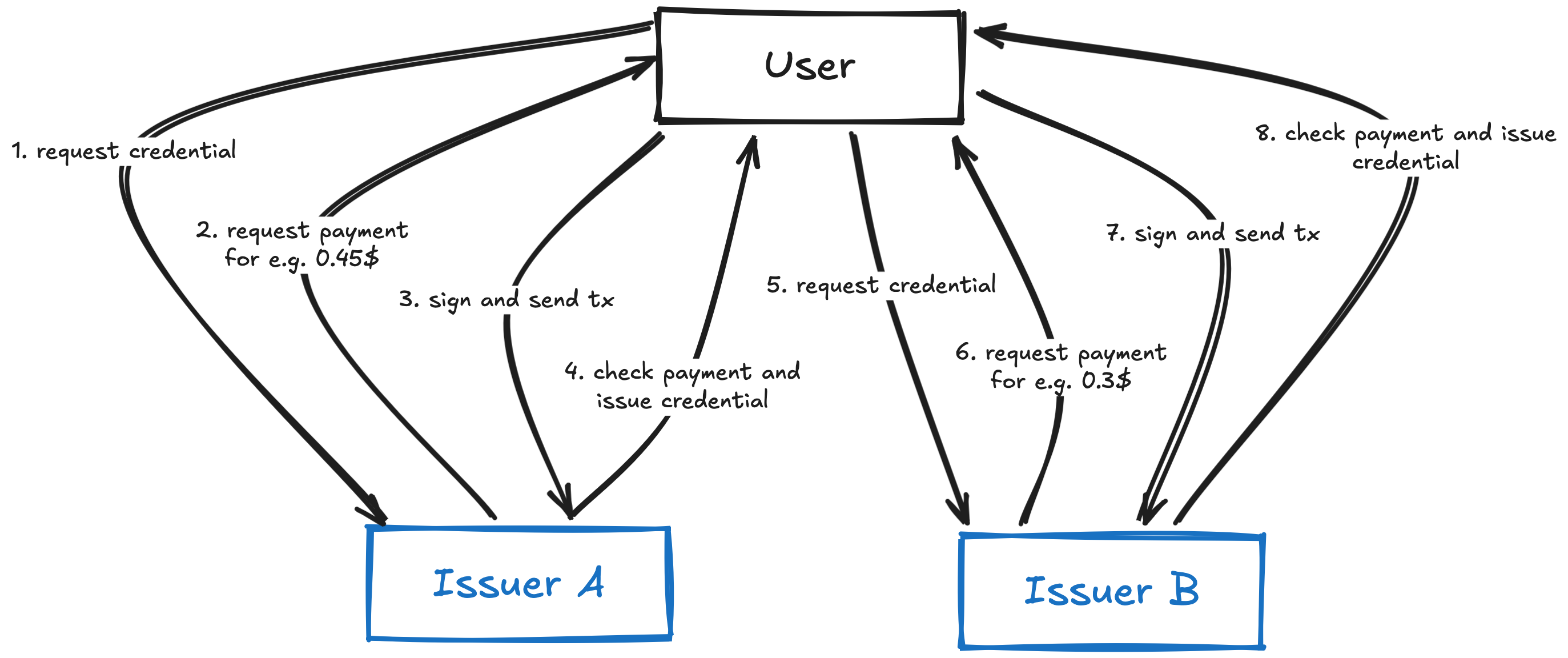

OIDCx402 flow (prototyped):

With OIDCx402, users can pay a small USDC amount to receive digital verifiable credentials. The payment is processed through the x402 payment protocol and the credential is issued instantly, without the overhead of traditional high fees and payment processing.

The key innovation is that payment becomes a native part of the credential issuance protocol rather than an external step. Users pay micro-amounts (often under $1) using USDC (or in the future any other asset), and the credential is issued instantly without the overhead of traditional payment processing.

Demo

Here's the full OIDCx402 flow in action — from credential request to payment to issuance.

Technical Considerations

Payment verification

One critical aspect is ensuring payments are verified before credential issuance. That's why x402 utilizes facilitators to verify that:

- The payment transaction was included in a block

- The correct amount was transferred to the issuer's address

Credential binding

Verifiable credentials should be cryptographically bound to their holder. In our implementation, we bind credentials to the same wallet address that made the payment, creating a natural link between payment and credential ownership.

Privacy considerations

While the payment happens on-chain (and is therefore public), the credential content remains private. The issuer only learns that a payment was made — the credential itself can be selectively disclosed by the holder later, or can make use of ZKPs to prove statements from the credential.

Further Improvements and Ideas

There are, of course, many improvements that could be made to the implementation, but here are some of the most important ones:

- Refunds: Define behavior for cases where the credential isn't issued successfully — the user should be able to get a refund; this is explored in the x402 docs as well.

- Batch payments: Allow users to purchase multiple credentials in a single transaction, then carry out the OIDC flow for those multiple credentials, reducing overall transaction costs and improving UX for bulk credential requests.

- Subscription models: Implement recurring payment flows for organizations that need regular credential updates or renewals (e.g., monthly compliance certificates).

- Dynamic pricing: Enable issuers to adjust credential prices based on demand, verification complexity, or user reputation scores.

- Escrow mechanisms: Hold payments in escrow until credential issuance is complete, providing additional security for high-value credentials.

- Credential marketplace: Create a discovery layer where users can browse and compare credentials from different issuers with transparent pricing.

- AI agent integration: Develop standardized APIs for AI agents to autonomously discover, purchase, and manage credentials on behalf of users.

- Pay-per-verification: There are use cases where users would want to pay for verification of a credential, and this could be done with x402 as well.

Conclusion

The OIDCx402 prototype shows a possible path toward making verifiable credentials economically viable for both issuers and users. By integrating x402 micropayments directly into the credential issuance flow, it eliminates the friction that traditionally introduces too much overhead for small payments, such as micropayments for digital credentials.

Beyond issuance, it also makes sense to consider micropayments for credential verification itself — paying a small fee only when a credential is used or verified. This model creates a more balanced and sustainable economy around digital identity interactions, where both issuers and verifiers are fairly compensated.

The implications extend far beyond simple payment processing. This approach also opens doors for AI agents to autonomously manage digital identities, enables new business models for credential issuers, and creates possibilities for digital credentials that were previously economically much harder to achieve.

While our hackathon prototype demonstrates the core concept, there are still many improvements and research directions to explore to make this approach more robust, scalable, and accessible to the broader digital identity ecosystem. As the world moves toward portable, verifiable digital identities, having a native monetization layer will be crucial for sustainable growth.

The future of digital credentials isn't just about technical standards — it's about creating economic incentives that make the ecosystem work for everyone. OIDCx402 is our contribution to that future.